Hey there,

This past Saturday, a few buddies and I crossed the border to catch a Detroit FC soccer game.

Great soccer, even better atmosphere – loud crowd, cold beer, and chicken wings for dinner. Basically a perfect afternoon.

On the way home, we passed through Old Walkerville.

I insisted we make a stop at the new Craig’s Cookies—I’d heard great things and figured gourmet cookies were the logical next step.

Only problem? We got there one minute after closing.

Brutal.

But for some reason, the lady working had a soft spot for a group of sad-looking, cookie-hungry middle-aged men.

She let us in…

And offered us a bag of the “not-so-pretty” cookies that didn’t make the display.

What a win.

Sometimes life throws you a break when you least expect it. lol

The Federal Election Is Coming

And if you’ve been listening to the noise, it sounds like the future of the country depends entirely on who wins.

Everyone’s picking a side.

Nobody’s really looking at the fundamentals.

But here’s what I believe:

Regardless of who wins next week, most of the things that will impact your long-term financial future won’t be changing.

So let’s take a step back from the political noise—and talk about what’s not going away anytime soon.

Government Debt Keeps Growing

This one’s not a partisan issue.

Debt is just the default operating mode of our federal government.

It used to be that “balancing the budget” was a key election promise.

Now? It’s seen as a pipe dream.

No one’s talking about paying the debt down—just managing the growth of it.

And when governments carry massive debt, inflation becomes a tool, not a bug.

Why? Because when prices rise over time, it makes the old debt smaller in real terms.

It’s like trying to pay off yesterday’s $100 tab with tomorrow’s cheaper dollars.

But that same inflation that helps governments hurts everyone else.

Cities Are Broke Too

Municipalities are in the same boat—but they can’t print money.

So what do they do?

They crank up development charges on new housing projects.

It’s politically safer than raising property taxes, but the effect is the same:

The cost of new housing goes up.

And that cost gets passed down to buyers and renters.

Higher-density projects—condos, stacked towns, laneway suites—are more profitable for cities.

So they get fast-tracked.

That means the traditional detached family home is slowly becoming a luxury product in many cities.

We’re not just in a housing crisis.

We’re in a housing transition.

When policy pushes more money into housing, prices rise. It’s been happening for decades—and the structure isn’t changing.

Affordability Gets “Fixed”… Then Broken Again

Every few years, the government rolls out a new housing policy to “improve affordability.”

Maybe they raise the insured mortgage limit.

Maybe they offer a new buyer incentive or grant.

And what happens?

Prices go up.

Then the system tightens up again. Affordability dips. New policies come out.

It’s a loop—and it rewards asset owners, while punishing anyone stuck on the sidelines.

Inflation Isn’t Going Anywhere

Nobody campaigns on the promise to lower prices—because they can’t.

At best, they aim to slow price increases.

But price declines across the board? Not going to happen.

Our entire system—from tax revenue to debt repayment—is built on inflation.

This isn’t conspiracy talk. It’s just the math.

It takes real policy courage to change that cycle—and no one in this election is proposing anything remotely close.

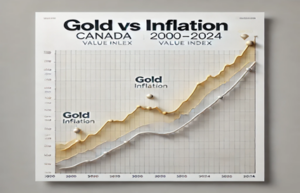

Cash in a savings account lost buying power, gold grew at over 9% annually. Real assets always win the long game.

Owning Assets Is Not Optional Anymore

The traditional idea of “save 10%, invest in safe stuff, retire at 65” is broken.

If your savings aren’t in assets that rise with inflation, you’re falling behind—quietly, but constantly.

That could be real estate. Could be business equity. Could be commodities.

But it can’t just be GICs and savings accounts.

That’s not to say you take unnecessary risk—just that you need a strategy that matches the world we actually live in.

So What Can You Actually Do?

This is where we come in.

We help investors, homeowners, and business owners get clarity on:

- How to finance the right properties

- When to leverage debt strategically

- And how to navigate a financial system that’s not built for average results

We don’t have control over elections, debt levels, or inflation.

But we do have control over how we respond.

Over how we plan. How we invest. How we borrow.

And who we surround ourselves with when it’s time to make important decisions.

Sometimes, even when you show up late for cookies…

You still walk out with a win.

Let’s make sure your financial game plan is built the same way.

Until next time,

Vince

P.S. If you’re thinking about a move—buying, refinancing, or just trying to make sense of where rates might go next—let’s talk.

P.P.S. Despite everything I said above, I still have very strong feelings about this election, and I encourage everyone to get out and vote.