Hey there,

Well, the Canadian Federal Election is over. The people have spoken. Mark Carney is now Prime Minister, leading a minority Liberal government.

Like many of you, I was more invested in this election than usual—probably more than I should have been.

Normally, I try not to get too caught up in politics. As someone who works in finance, I’ve always told myself:

“It doesn’t matter who’s in power. I’ll just adjust my strategy accordingly.”

But this time… it felt different.

Maybe it was how polarizing the campaign was.

Maybe it was what’s happening south of the border.

Maybe it was watching so many young Canadians struggle to buy a home.

Or maybe it’s just that I have young kids now—and I truly wonder what kind of future they’ll inherit.

Everyone was worried about something—but not always the same things.

Some were worried about Trump. Others about housing. Others about inflation, small business, immigration, education, jobs, taxes.

And honestly, they’re all valid concerns.

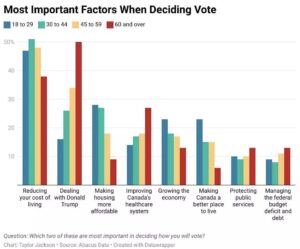

Just look at this:

The issues Canadians prioritized in this election varied sharply by age group. For younger voters, affordability dominated. For older voters, Trump took centre stage.

Because the truth is:

We’re all playing the same financial game. But the rules affect each of us differently.

And that’s what hit me hardest this week: The old system just doesn’t work anymore.

We were all sold a model: Go to school. Get a good job. Buy a house. Save money. Retire at 65.

But that formula doesn’t function in today’s economy.

Wages haven’t kept pace with inflation.

Asset prices have outgrown incomes.

And simply “saving” isn’t enough anymore—not when the dollar is quietly losing value every year.

So where do we go from here?

Let’s zoom out—because regardless of who’s in power, some financial truths don’t change:

Inflation isn’t going anywhere. It’s baked into the system. It helps governments manage their debt. But it chips away at your savings at the same time.

If you own assets, you’re ahead. Hard assets like real estate rise with inflation. They don’t just hold value—they build wealth. If you don’t own them, you’re working harder to stand still.

Smart debt makes a difference. Used properly, debt amplifies growth. It helps you control larger assets while preserving capital. It’s not about borrowing recklessly—it’s about borrowing strategically.

Interest rates aren’t random. Most people guess when it comes to fixed vs. variable, or term length. But when you understand what drives mortgage rates—BoC decisions, bond yields, lender pricing—you gain a real edge.

Education is everything. This is a system. And if you understand how money, debt, inflation, and capital flow actually work, you can stop playing defense—and start playing offense.

So yes, the election is over. And I genuinely hope this new government brings clarity, unity, and real results.

But for your financial future?

The winning strategy won’t come from Ottawa.

It will come from building a plan that works in today’s economic reality.

That’s where we come in.

Whether you’re buying your first property, scaling your portfolio, or trying to make sense of rates—we’re here to help.

Until next time,

Vince

P.S. Curious what this election might mean for interest rates, housing policy, or mortgage strategy? Stay tuned—next week I’ll break down where things could go next.